United: Proceed, with caution

United have maximised access to cash to improve negotiating power in the transfer market – performance on and off the pitch will still determine how much they can sustainably spend

United’s 2Q26 results showed the cost initiatives on both the player and non-player side have begun to take effect, an upturn in the club’s finances is now inextricably linked to Champions League qualification.

Revenue initiatives like increasing ticket prices have increased access to near term cash, as has pulling forward future monies owed to them.

Manchester United are taking a bet they are now better allocators of capital and using modern financing techniques to maximise access to cash today. This will improve their ability to negotiate for transfers (for instance, paying more money up front for a player).

Operationally, the club still has many areas to improve – the sacking of Amorim could not have been part of the plan. But they are operating with more financial discipline. The true alignment of a clear footballing strategy and financial discipline will see the Manchester United cash machine truly start to purr, eventually.

Mistakes proving costlier than thought

United will be booking an £6.3mn write off and a further £15.9mn provision related to the removal of Ruben Amorim and his coaching staff.

The £6.3mn write off relates to the balance sheet value assigned to Ruben Amorim. Recall United paid a fee to Sporting Lisbon for Amorim, this was amortised over the period of his contract (like a player transfer) and needed to be written down when he was removed from post. The write down suggests the fee paid for Amorim was closer to £11mn.

The total cost to hire and remove Ruben could total £26.9mn. Whilst I was expecting mistakes (they are inevitable in turnarounds), we should not forget the scale of these errors. Add in the cost to remove Ten Hag, hire and remove Dan Ashworth and we’re not far off the costly mistakes being the same as the annualised savings the cost cuts the club has made. Each of these costly mistakes eat into the turnaround budget. Operational excellence still needs to be exhibited.

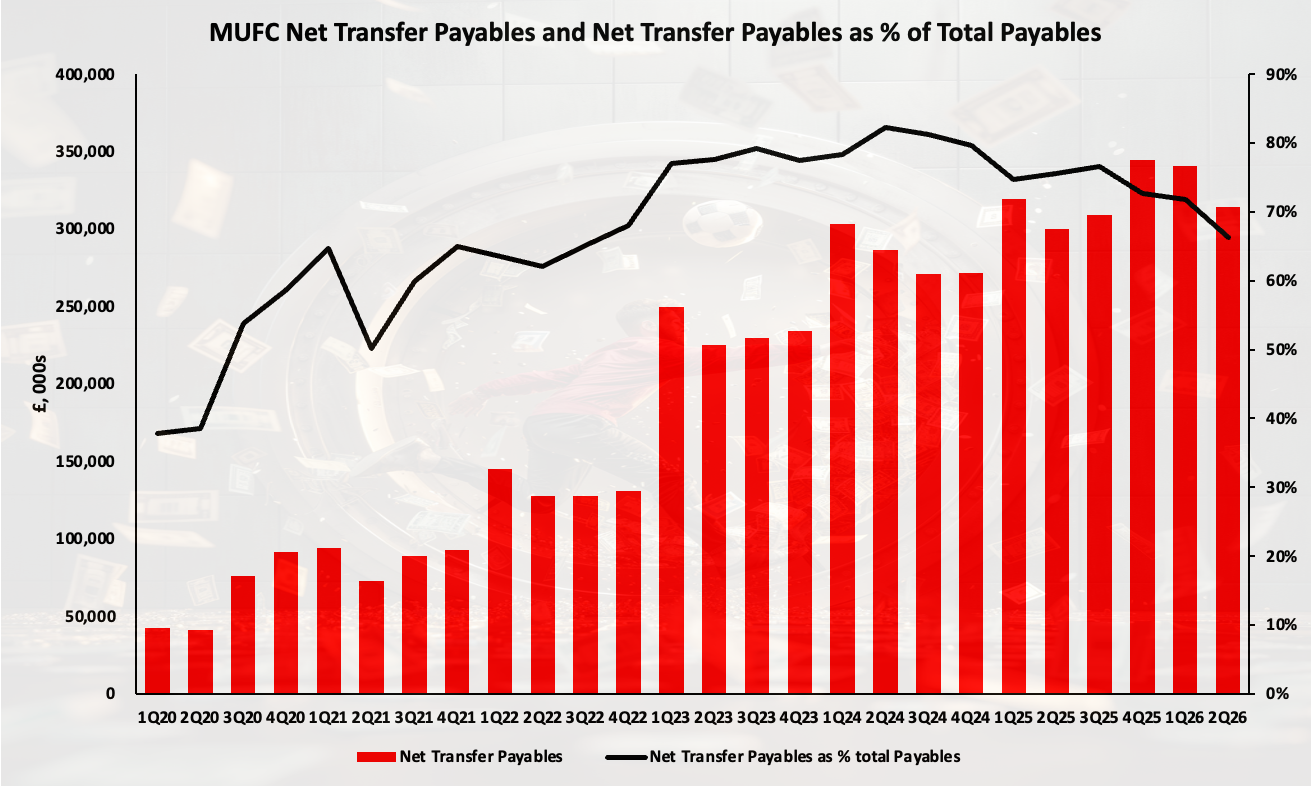

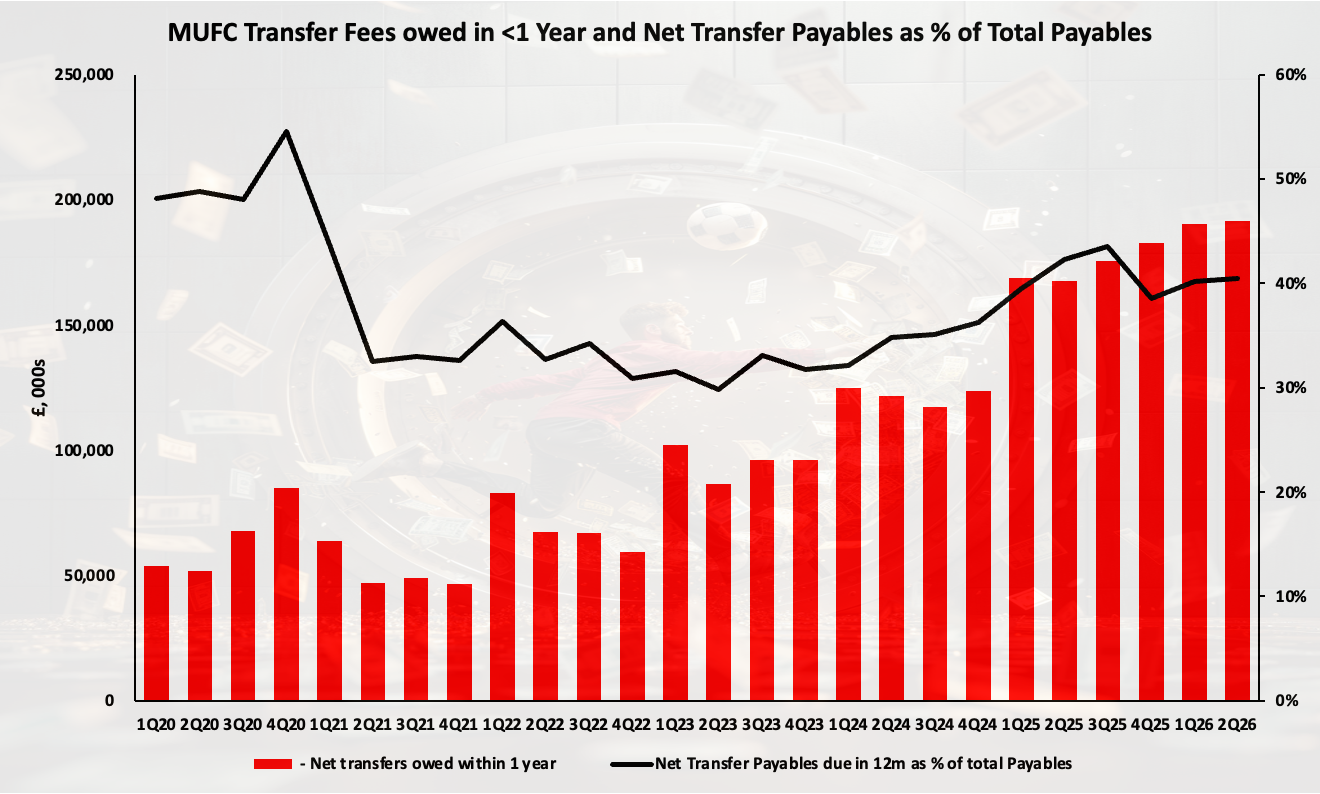

Near term net transfer debts will continue to take up most of the cash the club makes

United’s net transfer debt fell to £314mn in 2Q26. £190mn of that is still due in the next 12 months. United will be generating £190mn EBITDA this year and c.£250mn if they qualify for the Champions League next year. Most of this cash will still be used to pay down historic transfer debts. Whilst profitability and cash generating ability are improving, United are having to pull that money forward to allow them to act in the transfer market (see more below). They are still operating under constraints.

Source: Company data

Source: Company data

Ticket price rises, broadcasting revenue increasing ability to borrow

United increased the capacity under their revolving credit facility by £50mn in early February 2026. This follows a £50mn increase in July 2025. Typically, these sorts of facilities would be increased to reflect changes in the underlying financials of a company – you make structural improvements to profitability, banks are willing to give you that cash upfront because you know it can be paid back.

The previous £50mn was largely underwritten by the initial restructuring when INEOS took over day to day operations (£40-45mn annualised savings across FY25 and FY26).

So, how could United increase their borrowing capacity by another £50mn? The answer, I believe, lies in the multitude of other initiatives they have been implementing, some of which may catch the attention of fans:

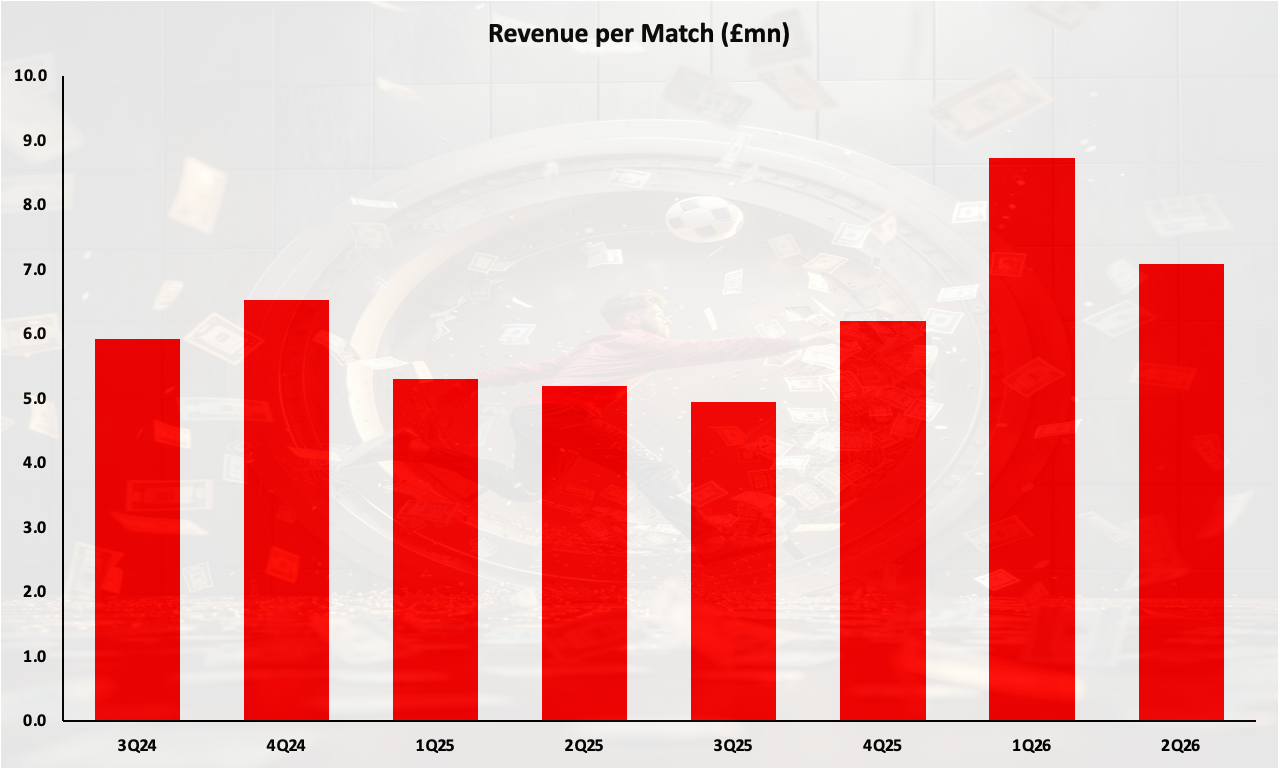

Matchday revenue: the price increases, new hospitality seats have all contributed to a 42% increase in revenue per match this season. United are averaging £7.5mn revenue per match this season. The presence of season tickets means one cannot extrapolate that growth to a season including the additional games in the Champions League. However, it will probably drive £15mn+ of incremental revenue per season.

Broadcasting revenue: whilst revenue per game in domestic tv rights is falling, international rights continue to grow (LINK). International premier league rights are now 57% of total media rights value and grew 25% in the last cycle. That could provide a £20mn+ revenue impact if United stay in the Champions League positions.

League position: we don’t know what forecasted league position the July 2025 credit facility increase was predicated on. Assuming it was a Europa League finish (per their financial guidance), a consistent top four finish as may be forecast in the future would drive an incremental £7-8mn.

Other operating cost reductions: the latest set of accounts showed other operating costs fell and equate to £5.4mn of savings on an annualised basis.

Source: Company data

Cash is king, and United are increasing their access to it

United disclosed they brought forward £39.4mn in transfer fees they are owed from other clubs in the future. This is not an uncommon practice in football, and is an increasingly cheap way to access cash today for clubs. What was more interesting is that these funds were almost entirely used alongside their cash reserves to pay down £50mn of outstanding debt on their revolving credit facility. Alongside the aforementioned reasons, this will have aided the expansion of their revolving credit facility.

But the net result of these moves is that United now have access to £185mn cash in their revolving credit facility. The £39.4mn of brought forward cash will still need to be earmarked to pay down transfer debts. But they have removed counterparty risk (risk they don’t get paid those funds), and increased their access to cash now – they are making a bet they are better allocators of capital. It doesn’t increase their ability to spend, but it gives them a lot more flexibility when negotiating transfers.